Understand EU CBAM: Your Export Compliance Guide

or complex compliance issues.

clearance and fund security.

Globally,addressing climate change and promoting a low-carbon economy have become undeniable trends.Among these,the EUs Carbon Border Adjustment Mechanism (CBAM) is a significant initiative aimed at ensuring that the EUs internal emission reduction efforts are not undermined by carbon leakage.So,as an exporting enterprise,how can you determine whether your products fall under CBAMs scope of control,and how should you respond to this new trade environment?

I.CBAM Regulatory Scope and Judgment Criteria

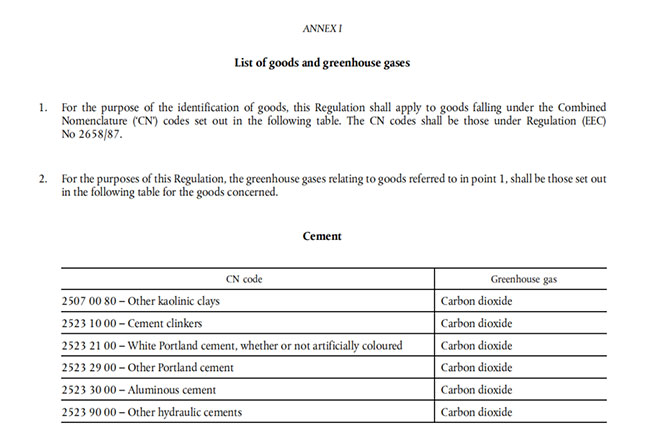

The implementation of CBAM is primarily based on the REGULATION (EU) 2023/956 legislation,which provides a specific list of controlled products in Annexes I and II (starting from page 39 of the regulation document PDF).Enterprises must first verify whether their products CN code is listed in the annex tables.If the exported products CN code is listed,it means the product is subject to CBAM control and must comply with the relevant regulations and procedures.

Regulatory Document:

II.CBAM Requirements for Enterprises

During the CBAM transition period,exporting enterprises must calculate the embedded carbon emissions of their products in accordance with official guidelines and implementation rules,and convey this information to downstream customers.This process involves quantifying direct emissions from the production process,including indirect emissions from electricity and other energy usage,as well as the embedded carbon emissions of raw and auxiliary materials.

III.Calculation and Tracing of Product Embedded Carbon Emissions

The concept of implied carbon emissions in products is similar to the carbon footprint of products,but its scope is smaller.The calculation of implied carbon emissions includes direct emissions (such as CO2 generated by the decomposition of calcium carbonate) and indirect emissions (such as CO2 generated by the use of electricity),as well as the implied carbon emissions of raw materials and auxiliary materials.For raw materials and auxiliary materials within the scope of CBAM control,enterprises need to trace their implied carbon emissions.In the absence of upstream supplier data,enterprises can temporarily use the default values provided by CBAM,but starting from July 2024,the emissions calculated using the default values must not exceed 20% of the total implied carbon emissions.

IV.Future Scope of CBAM Controls

As a supplement to the EU carbon market mechanism,the future regulatory scope of CBAM will align with the industries covered by the EU carbon market.It is expected that organic chemicals under CN code starting with "29" will be included as early as 2026,with efforts to encompass all industries or activities covered by the EU carbon market by 2030.

Was this helpful? Give us a like!

Contact our experts for compliance audits, precise quotes, and one-stop customs support.

Recent Comments (0) 0

Leave a Reply